快速查题-ACCA英国注册会计师试题

ACCA英国注册会计师

筛选结果

共找出50题

- 不限题型

- 不定项选择题

- 单选题

- 填空题

- 材料题

- 简答题

- 论述题

ABC is not a system that is suitable for use by service organisations.

Are the following statements about Activity Based Costing (ABC) true or false?

In a system of ABC, there is no under- or over-absorption of overheads.

Are the following statements about Activity Based Costing (ABC) true or false?

In a system of ABC, a larger proportion of overheads is attributed to low volume products than in a traditional absorption costing system.

The following statements have been made about activity-based costing.

(1) Unlike traditional absorption costing, ABC identifies variable overhead costs for allocation to product costs.

(2) ABC can be used as an information source for budget planning based on activity rather than incremental budgeting.

Which of the above statements is/are true?

Which THREE of the following statements about activity-based costing are correct?

(1) Implementation of ABC is unlikely to be cost-effective when variable production costs are a low proportion of total production costs.

(2) In a system of ABC, for costs that vary with production levels, the most suitable cost driver is likely to be direct labour hours or machine hours.

(3) Activity based costs are not the same as relevant costs for the purpose of short-run decision making.

(4) Activity based costing is a form of absorption costing.

Which of the following statements about activity based costing are true?

The following statements have been made about traditional absorption costing and activity based costing.

(1) Traditional absorption costing may be used to set prices for products, but activity based costing may not.

(2) Traditional absorption costing tends to allocate too many overhead costs to low-volume products and not enough overheads to high-volume products.

(3) Implementing ABC is expensive and time consuming

Which of the above statements is/are true?

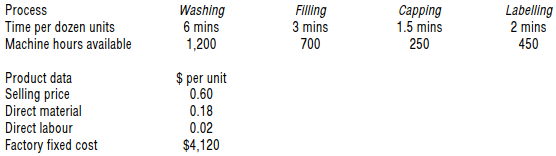

The following data refers to a soft drinks manufacturing company that passes its product through four processes and is currently operating at optimal capacity.

Which process is the bottleneck?

In which of the following ways might financial returns be improved over the life cycle of a product?

1. Maximising the time to market

2. Minimising the breakeven time

3. Maximising the length of the life cycle

In material flow cost accounting (MFCA), input manufacturing costs are categorised into material costs, waste treatment costs and which of the following?