Prepare the company's statement of financial position as at 31 December 20X4, complying as far as possible with IAS 1 Presentation of financial statements. Details of non-current assets, adjusted appropriately, should appear as they are presented in the question.

材料全屏

64

【论述题】

Prepare a statement of cash flows for the year to 31 December 20X2 using the format laid out in IAS 7,together with the relevant notes to the statement.

材料全屏

65

【论述题】

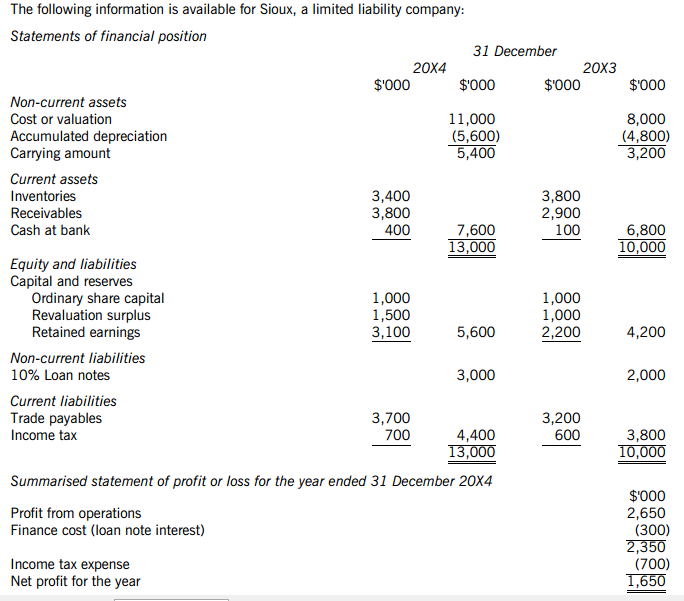

Prepare the company's statement of cash flows for the year ended 31 December 20X4, using the indirect method, adopting the format in IAS 7 Statement of cash flows.

材料全屏

66

【论述题】

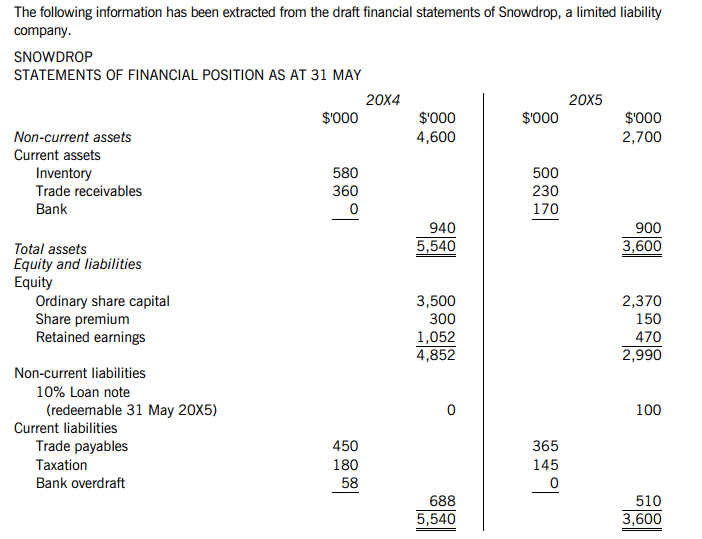

Prepare a statement of cash flows for Snowdrop for the year ended 31 May 20X5 in accordance with IAS 7 Statement of cash flows, using the indirect method.

材料全屏

67

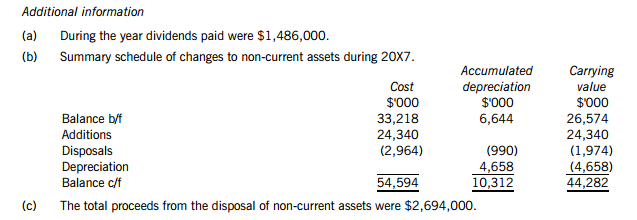

【论述题】

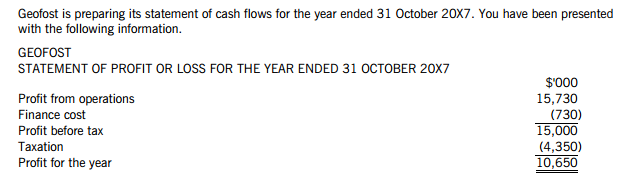

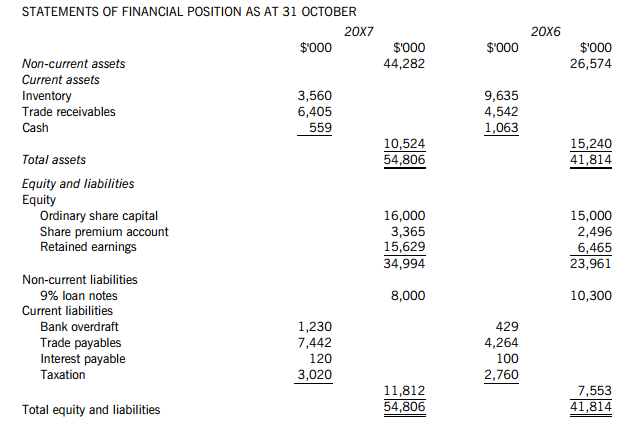

Prepare a statement of cash flows for Geofost for the year ended 31 October 20X7 in accordance with IAS 7 Statement of cash flows, using the indirect method.

材料全屏

12

【论述题】

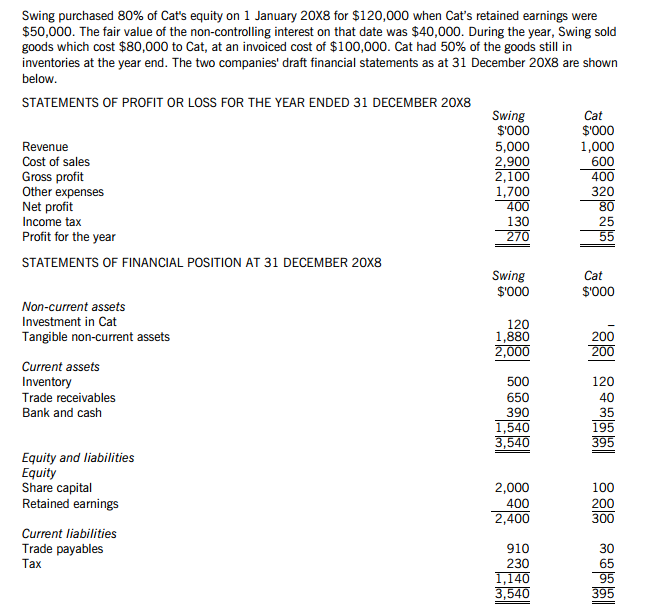

Prepare the draft consolidated statement of profit or loss and draft consolidated statement of financial position for the Swing group at 31 December 20X8.